Let’s pretend you’re Canadian.

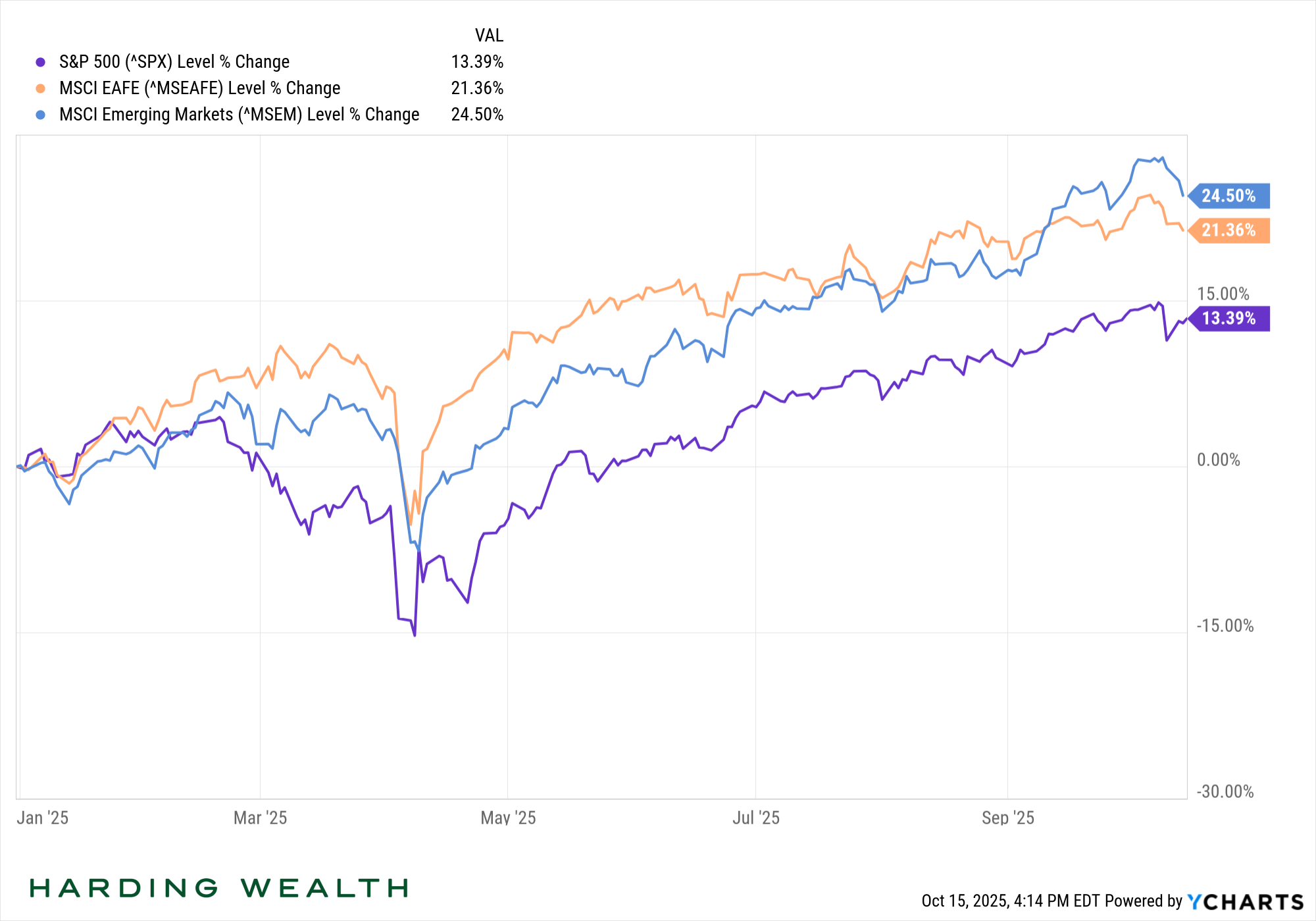

Non-US stocks are finally having their moment. Here’s their performance year-to-date.

*Past performance not indicative of future results.

[The orange line is international developed markets, the blue is emerging markets]

This is good. We like it when global diversification works in our favor.

But sometimes we can be a little biased towards our home country.

To illustrate this, let’s pretend you’re Canadian.

(If you’re actually Canadian, just sit back, relax, and be Canadian. No pretending needed, I like you just the way you are.)

You work, you earn money, you save, you invest… and you pick an investment strategy.

Let’s say you start out with an understanding of the equity premium — which is the premise that stocks will outperform cash and bonds over time, but (of course) not all the time — I think this is a smart initial assumption as long as you have the time and discipline to own stocks.

After you decide to own stocks, you put 50% of your stock investments into Canadian companies. It’s your home country, why not?

For reference, here are the 10 largest Canadian companies as of October 2025:

1. Royal Bank of Canada (RBC)

2. Shopify (SHOP)

3. Toronto-Dominion Bank (TD)

4. Canadian Imperial Bank of Commerce (CIBC)

5. Agnico Eagles Mines (AEM)

6. Thomason Reuters (TRI)

7. Bank of Montreal (BMO)

8. Constellation Software (CSCWF)

9. Bank of Nova Scotia (BNS)

10. Barrick Gold (ABX)

Perhaps you’re more diversified than owning only the top ten companies in Canada, but right about now you should be thinking “Wait. No Apple, Amazon, Nvidia, Berkshire Hathaway, etc. etc. etc.?! Why am I putting 50% of my stock portfolio into these Canadian companies?”

This seems especially odd when you consider that Canada is just the 6th largest stock market in the world and represents only 2.6% of the investable stock market, globally.

For good measure, here are the top 20 stock markets ranked, by size.

Source: Wikipedia

Okay, we can stop pretending now.

Based on a 2024 Study by Vanguard, Canadian investors had, on average, 50% of their stock investments concentrated in Canadian equities.

We call this a home bias. If there were no bias, the investor would only have about 2.6% of their portfolio in Canadian stocks.

Thus, the amount of the bias in this study is about 47.4% (the 50% representation of Canadian stocks in their portfolio minus the 2.6% representation of Canadian stocks in the global market).

You might think this doesn’t apply to you because you concentrate in US companies… Let’s talk about that.

The value of the US stock market is currently around $62.8 Trillion, which represents just about 50% of the $124 Trillion global stock market (https://www.visualcapitalist.com/124-trillion-global-stock-market-by-region)

Given the above, ask yourself this question:

Is it hypocritical to condemn a Canadian investor for having a 47% home bias if I would not criticize a US investor for having a similar home bias?

More exactly, an investor with 97% of their stock portfolio in US stocks would have about the same home bias as a Canadian investor putting 50% of their portfolio into Canadian stocks…47%.

And remember, you’re focused on wanting to produce a desired outcome (like retirement), so that should be the primary focus when it comes to investing your savings…. And that goal might mean you need to look outside of your home country’s stock market.

Let’s take a minute to look back at the 20 year period from 2005-2024. Here are various countries, ranked each year by stock market performance.

Notice the US being on top only once (2014):

Source: Dimensional

Look, if I had to pick a single country’s stock market to invest in it would be the US. But we aren’t confined to that.

When I talk about the need for international diversification, the two decades from 2000-2009 and 2010-2019 come to mind.

The “lost decade” from January 2000 through December 2009 resulted in disappointing returns for many who were invested in the securities in the S&P 500. The index that had averaged more than 10% annualized returns before 2000 instead delivered less-than-average returns from the start of the decade to the end. Annualized returns for the S&P 500 during that market period were −0.95%. Ouch.

However, see below how international stocks (7.07%/yr), international small cap value (13.7%/yr) and Emerging Markets (10.89%/yr) fared by comparison.

While 2000-2009 was definitely a tough period for US investors, 2010-2019 was certainly better with the US (S&P 500) leading the way.

After that decade of international and emerging market underperformance, it’s not surprising investors would want to concentrate in US stocks as a result. In fact, the narrative has shifted pretty significantly to “Why would I own anything other than a US Stock Index fund?”

Let’s consider the entire 20 year period?

As you can see above, for the whole period from 2000-2019 the US market didn’t beat any of the comparative indices in these charts. This reality may surprise some US-only investors.

So, Adam, what are you saying we should do?

This is just a blog, so I don’t give investment advice here (we reserve that for one on one conversation).

That said, here are some things to think about:

1) Don’t try to play the tactical game to duck in and out of exposure to certain countries. There’s just no way to consistently and reliably decide to do things like “buy Denmark (DNK) stocks” and then “Sell DNK and buy Hong Kong stocks” on a repeat basis.

2) Make a bet on progress. When your portfolio generally reflects the overall market you’re making a bet on the progress of the overall system. If you’re trying to weave in and out of investments you’re making a bet that someone else is dumber than you are. You’re smart, but I’ve yet to meet anyone who is unequivocally the smartest investor alive. Remember how smart the Nobel Prize-winning folks at Long Term Capital Management thought they were?

3) If you’re worried about other economies moving away from the dollar as a global reserve currency, international market exposure may help mitigate the risk of a weakening dollar.

(the above one is in bold because I’m getting this question A LOT. I have another blog in the works on this subject.)

4) It’s okay to have some home bias, just be sure to know that it’s there.

One last thing:

The Potential Upside of Bias

Holding an investment through the ups and downs is hard, and as a completely rational investor, it can be tempting to pursue a strategy designed to eliminate those ups and downs. This almost always comes with an opportunity cost.

But what if you could trick yourself into feeling better about holding the investment when things get tough? This is where your home bias may be able to help you.

To help illustrate this, let’s think about a literal home down the street from where you live. You buy this house as an investment, you can drive by it every day and you know the area well. It’s comfortable.

When the local real estate market gets difficult you are less inclined to panic — you know this market well, it’s literally in your backyard.

Does this mean your local real estate market is the best investment opportunity in the entire world to put your hard-earned savings?

The answer is: Maybe… if being nearby is what allows you to stay invested during tough times.

If feeling close to something helps with your investor psyche, then maintain a reasonable home bias. That may be concentrating more of your portfolio in US stocks because you know the system and believe in it. This is totally reasonable. But know I’m always going to encourage you to hedge against the possibility that you’re wrong.

That’s all for now.

Onward,

Adam Harding

CFP® | Advisor | Harding Wealth

Chat with me

*past performance is not indicative of future performance. For educational purposes only.

Dimensional study: https://my.dimensional.com/a-tale-of-two-decades