The Answer You Hate

If you’ve worked with me for a while, you tend to know what the answer to some of your questions is going to be.

“Adam, are you worried about a crash?”

And I give the responsible answer.

Crashes are unpredictable. Markets price in information quickly. We don’t try to time recessions. We stay diversified. We think long term. History shows recovery.

It’s all true. It’s also wildly unsatisfying for both of us.

(Believe me, I am as tempted as anyone to start weaving narratives about why this time is different.)

Look, artificial intelligence feels disruptive in a way that’s hard to model. Geopolitical tensions feel different this time. Debt levels are high. Political rhetoric is loud. It feels like cracks are starting to form.

I know you don’t want a lecture on 2008 or 1999 or 1973 or 1929.

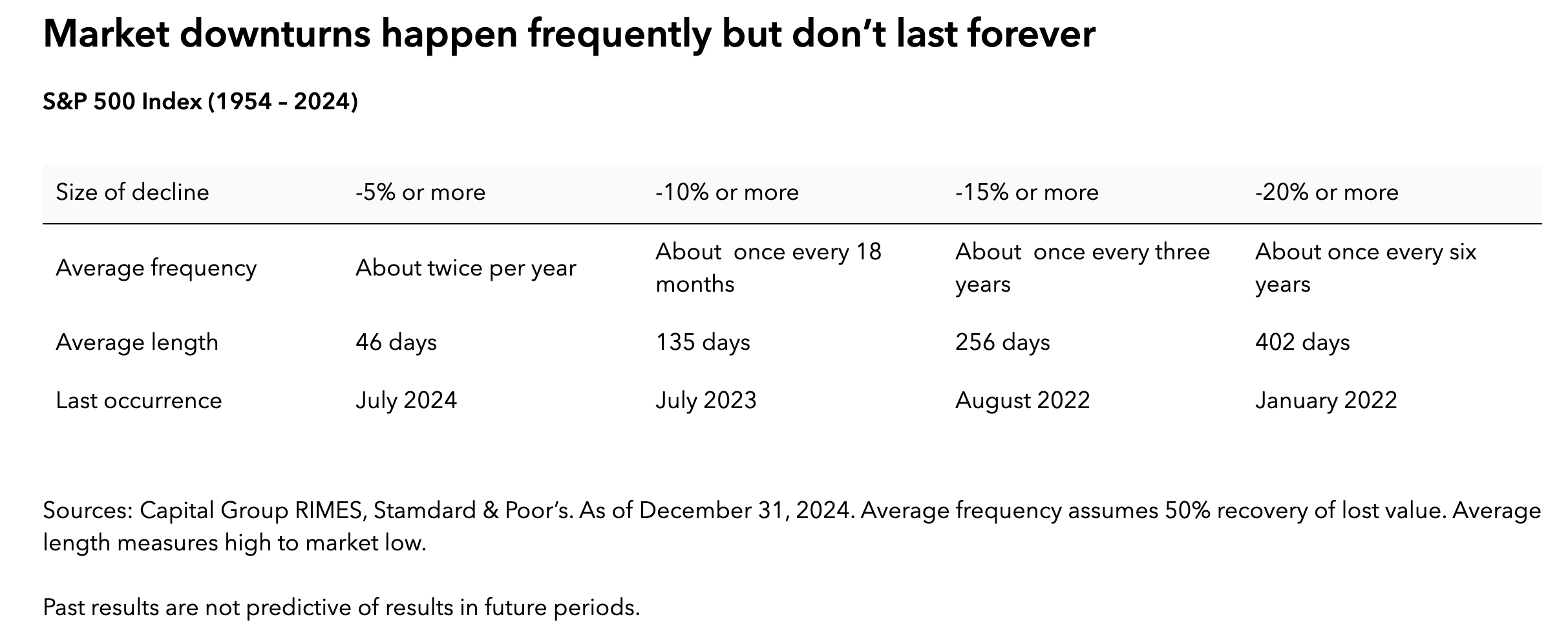

You don’t want me to give you this data about the frequency of market declines.

You want to know: What if the future really is different?

So let’s imagine something radical.

Pretend There Is No Past

Imagine the markets are being created today.

There are no charts. No long-term return data. No history of resilience. No case studies of recovery.

All we have is the future.

The first thing you have to acknowledge is the most important:

Everything is an “investment decision”… And deciding not to invest in stocks, bonds, or real estate is a decision to invest in cash.

Everything must be owned. When you reframe selling stocks or selling real estate as “buying dollars” it can take on a bit of a different light.

Okay, now let’s play it forward.

1) The Engine of Disruption

The two main headwinds clients seem to be worried about are Artificial Intelligence and Geopolitical Conflict.

Artificial intelligence could (will) replace jobs, create entirely new industries, shift profit pools and redefine national competitiveness.

Geopolitical realignment could reshore supply chains, fragment trade, reprice energy and commodities, and reshape defense spending.

In a world like that, what would you want to own? Seriously, don’t wait for me to make the argument for anything. Just ask yourself what you think is best. Maybe write it down.

(Space left intentionally blank to allow you to actually write it down)

Okay, now that you have your answer, I’ll give something to think about.

If you have savings, a portfolio, and a good income, then there’s nothing keeping you from broad ownership of the productive engine of the world.

If you’re like me, you can hate that people will lose their jobs to AI. You can hate that people who have families and mortgages and healthcare to buy are diminished down to replaceable inputs to production and are easily expendable in pursuit of profit. But you can also realize that you’re a person with a family and housing and healthcare to buy.

This is the system you’re in. Disruption does not eliminate capitalism — it reallocates profits within it. Might as well capture some of it while your fingers are crossed for our collective future.

Simply put, if AI or Geopolitics change everything, someone earns the returns.

…If supply chains move, someone builds them.

…If defense spending rises, someone supplies it.

…If productivity explodes, someone captures the margins.

Owning global businesses is not a bet against disruption.

Note that I said “global” — this expression of humility acknowledges that the US may not always be the best thing. That the Dollar may not always be the global reserve currency. More on that:

2) Don’t Assume the United States Wins Every Chapter

The U.S. has been an extraordinary place to invest.

But if we’re pretending there is no history, we wouldn’t assume:

The U.S. remains the dominant economy.

The dollar remains the unquestioned reserve currency.

Innovation is permanently concentrated in Silicon Valley.

AI research is global.

Capital flows are global.

Demographics are different across regions.

Political systems respond differently to stress.

If we were building the market from scratch today, would we really say:

“Let’s put almost everything in one country.”

No chance.

We would want ownership across Europe, Asia, emerging markets — not because we distrust the U.S., but because the future does not belong to a single flag.

3) Own More Than One Currency

If geopolitical tension escalates, currencies move.

If fiscal policy strains, currencies move.

If energy trade fragments, currencies move.

If reserve status shifts, currencies move.

Owning assets denominated in multiple currencies isn’t speculation.

It’s structural resilience.

If you only own dollar-based assets, your entire purchasing power is tied to one monetary regime.

If you own global businesses that generate revenue in euros, yen, francs, pounds, yuan, and dollars — you have exposure to multiple economic systems.

So What About the Crash?

Now we can circle back to the original question.

“Are you worried about a crash?”

If by crash you mean a 20–30% market decline — those will happen. They are the cost of admission.

But the more interesting question is this:

If the world changes dramatically over the next 10–20 years, do you want to be a spectator… or an owner?

If AI reshapes labor markets, if geopolitical blocs harden, if industries rise and fall — broad, global ownership means you participate in the reallocation of capital rather than trying to predict it.

The future might look nothing like the past.

That’s precisely why owning the productive assets of the world — across countries and currencies — remains rational.

Ownership is how you participate in whatever future actually arrives…. And if you are a benevolent, or perhaps even reluctant owner, we need your involvement perhaps now more than ever.

That’s all for now.

Adam Harding