Fight After School.

When I was in fifth grade I got in a fight.

Here’s what happened:

At one of the school recess breaks I was running around the playground and a kid, Dylan, and I ran into each other. One of us said something along the lines of “watch where you’re going”… and that was all the crowd needed to take things and run with them.

One kid suggested we fight.

Then another bystander seconded the idea.

Then another.

Within a few minutes it was settled — it would go down at 3pm around the far side of the school where the teachers and adults wouldn’t spot us. Dylan and I said nothing but just sort of nodded our heads like “okay I guess”. But, hey, this was 1994 and I was wearing a No Fear shirt. I was ready.

As the clock raced towards the closing bell, the pressure mounted.

The bell rang.

The parents picked up the kids who needed a ride home and the remainder (the kids who lived close enough to walk home) stayed for the show.

I walked around to the side of the school and everyone was there. They circled us and we fought, reluctantly, while also not trying to seem weak to our peers.

This was back in the early 90s, so our fighting inspiration was Karate Kid and other movies of that era. This was not mixed martial arts. Picture two little knuckleheads trying to land roundhouse kicks.

The fight ended after a couple minutes of this and no injuries other than some scrapes and bruises.

The crowd dissolved, everyone went home, and that was it.

[Before I tell you why I’m telling you this, just know that Dylan and I became friends after. Funny how that works.]

So why am I telling you this story?

…Because the crowd often demands things with complete disregard to those actually in the arena with something at stake.

This is rampant in investing decisions.

“BUY SPACEX”

“BUY GOLD”

“BUY BITCOIN”

“INVEST IN RENTAL PROPERTIES”

“BUY INDEX FUNDS”

The problem with this? None of it has context.

Here’s another story:

A couple weeks ago I was sitting in the coworking space at my gym and a woman (who had seen my Harding Wealth water bottle and assumed I was an advisor) asked what I thought about her rental property. Should she sell it? Should she raise rents? Should she 1031 Exchange into another property? etc.

Before I could give the appropriate answer (which is “It depends” followed by a bunch of other questions), a fellow member of this coworking space whose profession was Loan Officer chimed in with his expertise:

Him: “What’s your interest rate?”

Her: “3.5%”

Him: “Definitely don’t sell.”

Her: “Yea, I get that the rate is good, we just have some other things we could use the equity for—”

Him: “Yea, but you NEVER give up a rate like this.”

…And then he started talking about home price appreciation at 5-7%/yr like it was a guarantee.

I didn’t interject, let them have their conversation, finished the email I was working on and then went up to the weight floor to hit my workout. But again, the problem here is context-less decision making.

…What if this woman has high interest debt to pay off?

…What if the return on equity is barely worth the headaches associated with owning and operating a rental? (this is very common right now).

…What if her kids are getting ready to go to college and they don’t know how they’re going to afford tuition without tapping this equity?

In this situation, there are a bunch of questions to ask after saying “It depends”…. The context is required.

Money = fuel for your life. Nothing else.

Clearly define what your life looks like today and how you want it to look at various points in the future and the investments will fall into place.

Don’t let someone else pick your fights for you.

One final note about IPOs in light of the big ones coming down the pipeline.

First, let me acknowledge something: I know I’m not fun.

IPOs, Crypto, Tactical Market Timing, Blackjack, Powerball, Sports Betting? All fun. Also, all things I don’t do.

But I think it’s important that you know I was not born this way. I didn’t enter this world looking for milk and then immediately suggest IPOs don’t belong in a reasonable portfolio. I learned it.

Some research to support that:

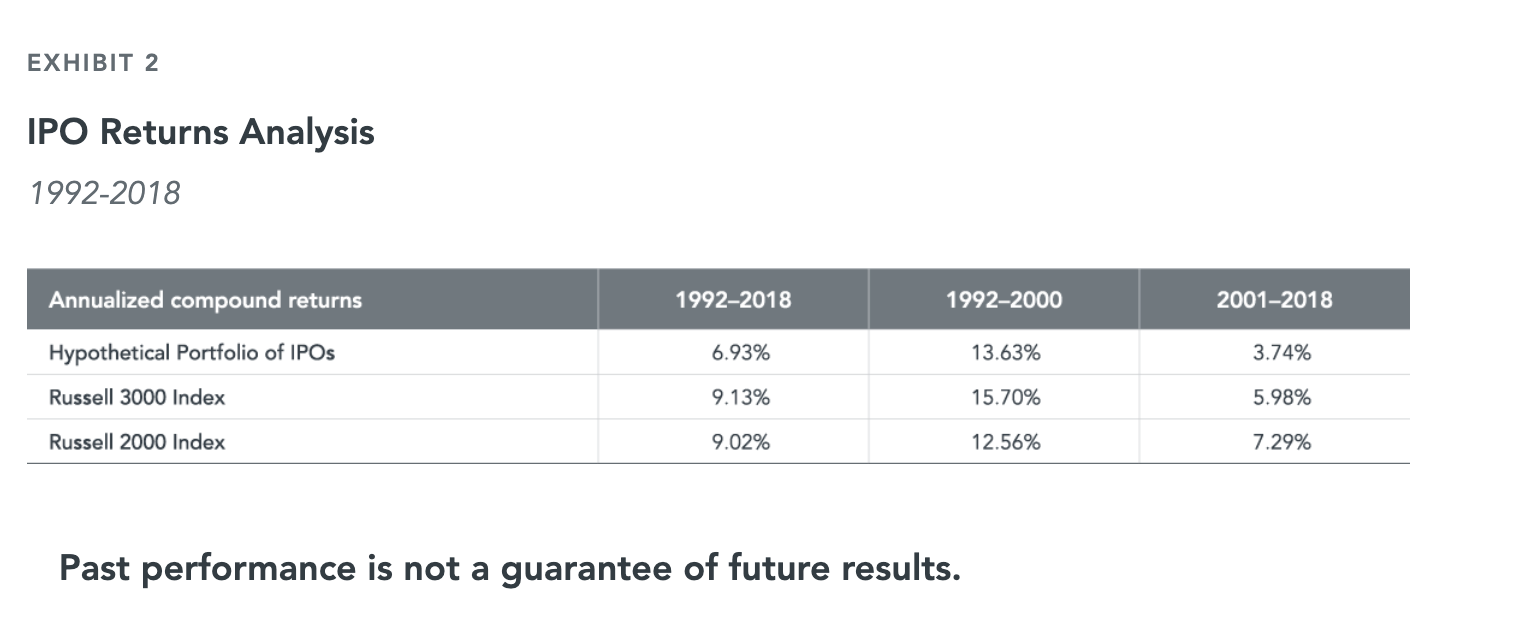

Back in 2019, Dimensional evaluated IPO returns by forming a hypothetical market cap-weighted portfolio consisting of IPOs issued over the preceding 12-month period, rebalanced monthly. This methodology excludes the initial first-day returns by design to alleviate the adverse selection problem inherent in the IPO allocation process. The table below compares the returns of the IPOs to the returns of the Russell 2000 (e.g. “small US Stocks”) and 3000 (e.g. “the entire US stock market”) indices over the full sample period as well as two subperiods covering 1992–2000 and 2001–2018.

You guys, this was the absolute heyday for IPOs.

As you can see IPOs as a group underperform the Russell 3000 Index in both the overall period and sub-sample periods.

For example, IPOs generated an annualized compound return of 6.93%, 13.63%, and 3.74% over the full, initial nine-year and final 18-year sample periods, respectively, as compared to 9.13%, 15.70%, and 5.98% for the Russell 3000 index over the same time horizons. In comparison to the Russell 2000 Index, the hypothetical portfolio of IPOs underperform in the overall period (6.93% vs. 9.02%) and the 2001–2018 (3.74% vs. 7.29%) subperiod and outperform (13.63% vs. 12.56%) over the period from 1992 to 2000.

Why might this be?

IPOs often behave like small growth, low profitability, high investment stocks, which have had lower expected returns than the market. But this is a technical explanation… Instead, let’s do this in everyday terms and go back to the story of the mortgage bro and the lady at my gym asking about her rental.

…Let’s say her rental income is $2,500/mo and her mortgage/taxes/etc. are $1,000/mo.

…And we initially guess that her property is worth an estimated $500,000 and she owes $200,000.

Her $300,000 in equity generates $18,000/yr in net rental income — a 6% yield with some upside potential from price appreciation.

(for the sake of brevity, let’s set aside the reality that once every 5-7 years there’s likely to be a thing or two that wipes out that $18,000: Roof, A/C unit, etc.).

We know that 20 Year US Treasuries are currently paying about 5% with pretty minimal upside potential.

So, with this information related to cash flow, we can dial in a price we think is fair (probably higher than $500,000).

With IPOs, however, the pricing gets messy. A lot of it is based on the hopes and dreams and stories and fables of future riches born out of endeavors which may or may not pan out. And the more obscure the cash flow picture (or absent, in the case of “assets” like crypto), the harder it is to know what something is worth.

So, with that, I’ll leave you with one final thing to remember:

When you buy investments, someone is selling them to you. So if you rush out to buy an IPO over the next several weeks/months, think to yourself “who is selling this to me?” and ask yourself WHY? …. They probably know more about the investment than you do.

That’s all for now.

Onward.

AH

*For informational purposes only. Not investment advice.