10 years.

I started this firm 10 years ago…

…well, 9 years, 10 months and a few days, actually.

It’s been so damn fun.

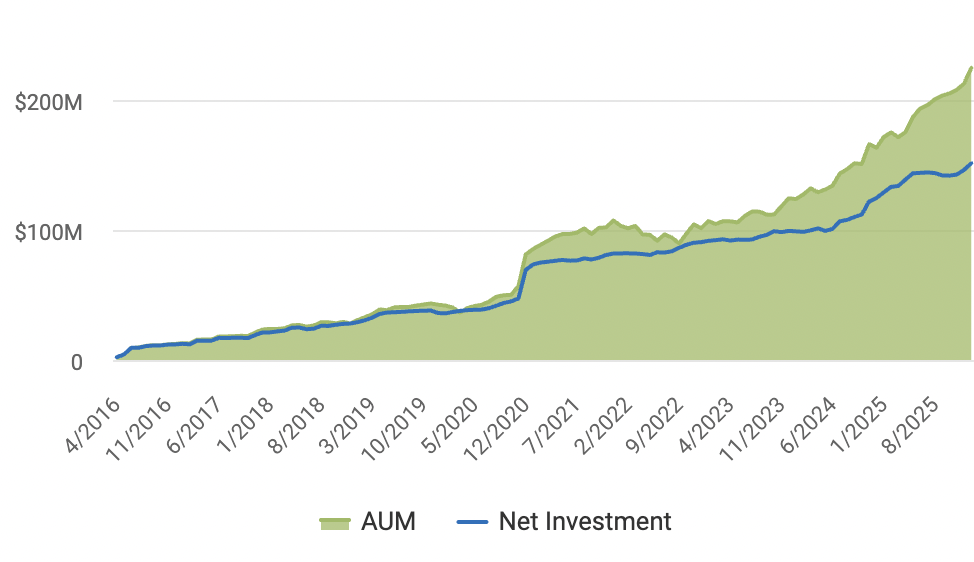

From 0 to 170 families.

From 1 to 5 employees.

From $0 to north of $230 million entrusted to Harding Wealth:

(Not an indication or advertisment of investment performance.)

I’ve been thinking a lot lately about those early days.

Specifically, the wonderful balance between fear and optimism that exists at the onset of taking risk. In hindsight, success tends to make that early fear seem less than it actually was. (Markets do the same thing. How many of you have muttered “of course the market came back” when thinking about the Covid crash in 2020?).

Still, the upside of that fear is materialized in the many retirement celebrations, family vacations, and worry-free nights enjoyed by our clients. But, of course, there have been a few sleepless nights, some vacations forgone because life had other plans, and some loss along the way. This is how it works.

I’ve welcomed my own three kids over that span and I can’t help but think about how having money literally means there’s at least another human life or two in my own family. You see, we’re a bit too practical to just have a bunch of kids and not think about the costs of everyday things and how stretched a budget can be. After 10 years, we’re fortunate to not have to worry as much about the skyrocketing cost of berries (or whatever).

That experience also shaped the kind of advice I’m giving, so I’ll spend the rest of this blog talking about that.

Recently, I was speaking with the adult daughter of long-time clients. I asked whether she planned to have kids.

Her response was rational: she wasn’t sure if it was in the cards for her after considering daycare costs, career momentum, retirement savings targets. You know, the math of modern life.

But aside from that, she wants children.

Meanwhile, her parents — in their mid-70s — have several million dollars invested with us. Wealth built through decades of discipline, risk-taking, and staying the course. When I talk to them, they light up at the thought of grandchildren.

They simply haven’t opened up about this with one another.

We can say with a high degree of confidence that the parents will have more than enough — including resources for assisted living or long-term care. We actively encourage them to enjoy their money: take the trips, order the good wine, buy the dream car.

And we’re also confident there will be a substantial inheritance.

The timing, however, is the issue.

Inheritances often arrive in someone’s 50s or 60s — long after the window to have children has closed.

If you’re in the younger generation, it can feel uncomfortable to ask for help. If you’re in the older generation, it can feel risky to give money away that you might need later. Both reactions are completely reasonable.

Every family is different. Different personalities. Different spending habits. Different histories. There’s no one-size-fits-all solution.

But I don’t believe helping your kids afford to have kids is “spoiling” them. This isn’t underwriting a luxury car. It’s underwriting your future family.

If you’re not ready to share the complete details of your financial life with your kids, I get it. You don’t need to.

Sometimes the starting point is simple:

“If you decide to have children, your father and I would gladly cover education costs.”

Or:

“We’re comfortable helping with childcare in those early years.”

That kind of clarity can change everything.

If you’re younger, I’m not suggesting you bank your entire retirement on a future inheritance. That’s neither wise nor empowering. But completely ignoring a very real and highly probable part of your financial picture isn’t rational either. Good planning acknowledges reality — even when the topic is delicate.

Money is ultimately about optionality.

Yes, going to Europe for the eleventh time is wonderful.

But so is your four-year-old granddaughter grabbing your hand while you cross the street on a random Tuesday afternoon.

One experience compounds memories. The other compounds generations.

The fear of “what if we need it later?” is real. So is the regret of “what if we waited too long?”

After 17 years in wealth management and ten years of watching Harding Wealth clients build wealth, protect it, spend it, and pass it on, I’ve come to believe this:

The best financial plans don’t just maximize net worth. They maximize life.

Over the next 10 years of working with clients, our success will be measured by how well we use our technical expertise to explore these kinds of grey areas to help focus on what really matters.

That’s all for today.

Adam

Advice @ Harding Wealth | Father of 3, including a freshly-turned on year old (pictured)